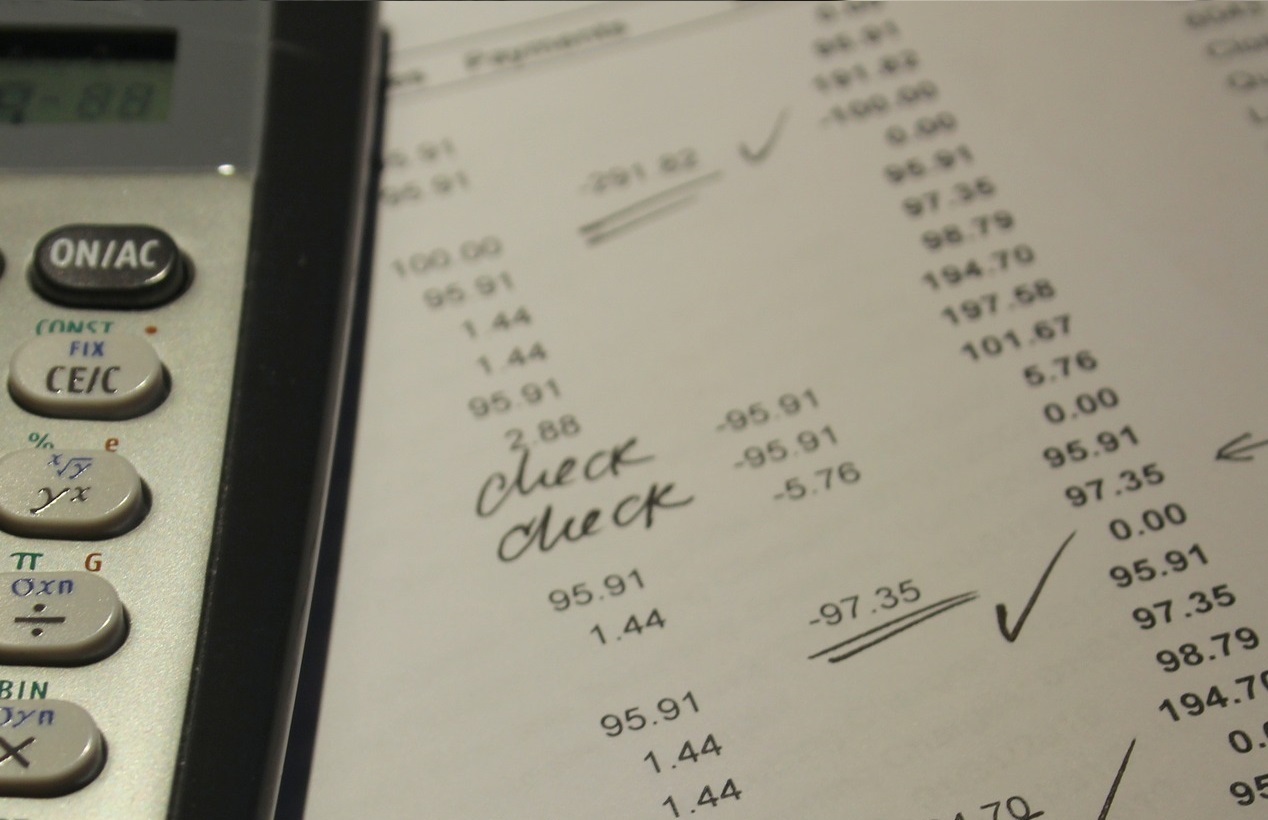

You Better Reconcile

When we meet with new clients, one of the first things we like to determine is how recently their books have been reconciled to the bank accounts. Sometimes, (rarely), the books have been reconciled to the prior month. Sometimes it's been a few months, or a few years. Sometimes a bank reconciliation has never been performed, and the client's not really even sure what that means.

Since "knowing is half the battle", I'm going to explain what a reconciliation is, the basics of how it's performed, and why it's important.

What's a monthly bank reconciliation?

To clarify, there are many types of reconciliations, for bank accounts, credit cards, petty cash, inventory, sub-ledgers, etc. For this article, we're referring to bank reconciliations. A bank reconciliation is like balancing your checkbook, for your business. Most accounting software programs now come with a reconciliation tool (instead of the spreadsheets we used in the days of yore). Since it is the most popular accounting software in small business, I'll be referencing the QuickBooks reconciliation tool.

How is a reconciliation performed?

First, you need to see when the account was most recently reconciled, and then obtain a copy of the bank or credit card statement for the following month. Second, after ensuring that the prior month's ending balance matches the following month's beginning balance, you'll note the statement's ending date and ending balance.

From there, you go line-by-line through that month's transactions, matching each one to its equivalent entry in your accounting software, to make sure that all transactions are properly entered and that your cash balance in the software matches the balance in the bank, for the same ending date.

That sounds very time-consuming and tedious. Why would anyone want to do that?

Monthly bank reconciliations are a very useful tool for ensuring accuracy in your books. They can:

Show you what's missing. Sometimes, transactions do not make it into the books, either because they did not download correctly, or weren't manually entered. If a transaction is on the bank statement but not in the software, you know it needs to be added. Also, sometimes there will be things recorded in the software which aren't on the bank statement. These could be inaccuracies, or it could be something like checks which have not yet cleared the bank. If there's a large number of uncleared checks, it's helpful to know that, for cash-flow purposes.

Show you what's duplicated. If you have a large number of uncleared checks, particularly if some of them are months-old, it could mean that an expense was added without being matched to the written check, and was therefore duplicated. The same thing can happen with income. I once found where a new client's prior-year annual sales were overstated by about $50,000, due to deposits not being matched to previously-recorded payments. The uncleared payments showed up on the reconciliation report, and helped the client avoid overpaying on his taxes.

"Lock down" errors to one period. If your books were accurately reconciled last month, and something is wrong on this month's bank reconciliation, you only have to go through about the last 30 days to find the error. If your books have not been reconciled in a long time, or ever, it's going to be a lot more work to find where the inaccuracy occurred.

Maybe accounting professionals are a little weird, but many of us even find bank reconciliations to be fun (or, at least very satisfying when accurately completed). If you're having trouble with your bank reconciliations, if you need help learning how to perform them, if something looks wrong but you're not sure what, or if you're just sick of doing them and want to pass the job off to someone else, contact us. We happily provide a free 1-hour initial consult to answer your questions.

What to Look for in Hiring a Bookkeeper

As your business grows, you will reach a point where you need to seriously consider hiring a bookkeeper. Unfortunately, bookkeeping is still a very un-regulated industry. Anyone can market his or herself as a bookkeeper, and it can be very difficult to sort the wheat from the chaff.

Obviously, your needs will be very specific to your company. However, there are a few basic things you can look out for to help you make the best decision in hiring a bookkeeper.

Look for certifications AND references.

Some people are very good at test-taking, and can certifications easily in an afternoon. (For instance, some lower-level QuickBooks certifications can be very easy to obtain with a minimal amount of studying.) But if they are difficult to work with, or don't do a great job of taking care of clients' books, they will likely not have many positive references available.

Some bookkeepers are very social and, at least on the surface, can impress clients. (Or, at the very least, they're good at getting friends and family to provide them with references.) However, if they do not have the accounting knowledge and technical skills necessary, they won't be good bookkeepers.

When seeking help, prioritize bookkeepers who have both certifications and a significant amount of references. Beyond client reviews, also look for reviews from partnering businesses, such as CPA firms. A good CPA appreciates working on financials that have been prepared by a good bookkeeper.

You can also ask your potential bookkeeper for references from current or prior clients in a business similar to yours.

Check their business registration.

Most legitimate bookkeeping firms will have officially registered their company. Depending on their state of registry, you can look up such information as how they are structured, how long they have been in business, their company officers, whether they have every faced dissolution, etc. (In North Carolina, where we're based, you can check the Secretary of State website for business registrations.)

There's nothing wrong with hiring a newer company, but you might want to consider a bookkeeping firm which has been in business for a few years, first. You can also look at things like whether they have a physical office space, or if the company ownership has changed hands multiple times. (And if they have been administratively dissolved in the past, consider it a major red flag.)

Heed the red flags.

There's a great quote from the show Bojack Horseman which goes, "When you look at someone through rose-colored glasses, all the red flags just look like flags."

Considering the high importance of your bookkeeping being done accurately, you do not want to ignore any red flags in your search for a bookkeeper. Being slow to respond, having little web presence, or being too eager to jump into working with you can all be red flags. If they are setting off your alarm bells during the initial search, consider how much worse things can become once you have hired them.

Ask about their experience with companies like yours, and with services you might need (such as their systems for managing payroll, sales tax, etc.). Ask about their policies on client communication, and how they prioritize time-sensitive tasks. Most importantly, particularly if they are a 1-person shop, ask about their plans for who can back them up on your account in the event of an emergency, where they might be unexpectedly unavailable.

Make sure THEY ask YOU good questions.

A few months ago, we met a prospective client for a free 1-hour consultation. She was upfront about the fact that she had scheduled interviews with other bookkeepers, and would be following up with us later. A few weeks later she let me know she would like to hire us. Her reason for choosing us, over other companies was, "You actually asked me questions and looked at my system. You were the only one who did that."

Be leery of a bookkeeper who swears they can handle your business financials without first establishing exactly what that entails. Not every client is a good fit for every bookkeeper (and vice versa). We maintain friendly relationships with our local competitors, so we have a good alternative to offer when we meet with a prospect and realize they would not be a good fit for us. Likewise, our competition sends us referrals, as well.

In your initial meeting with your potential bookkeeper, make sure they are trying to learn about your business, and not just sell you on theirs.

Find someone who understands accounting beyond record-keeping.

There is a misconception that a great bookkeeper is just someone with exceptional data entry and organizational skills. However, there is a lot that a real bookkeeper can do to help save money on taxes, identify areas of risk, or even improve profitability. Something as simple as how an owner's cash contribution to the company is recorded can have a massive effect on tax liability. A good bookkeeper can also locate missing accounts receivable, or locate credit balances with vendors. There's so much more to it than entering transactions from the bank feed.

Hiring a bookkeeper is one of the most important decisions you will make for your business. Be sure to take your time and be intentional in your search.

Staying (Financially) Fit Over the Holidays

With Halloween only 12 days away, we are officially in the holiday season. This is my favorite time of year, and I understand the temptation to let work slide as I give into the distraction of Thanksgiving, Christmas, and vacation.

But holiday season coincides with year-end and, for businesses, this needs to be a time of focus. Just as it's easy to undo months of dedicated diet and exercise with the wild abandon of the holidays, it's easy to let your business financials slip at the time when you really need them at their peak.

Here are a few common bookkeeping issues we see in Q4 year after year, and how to avoid them.

Missing Deductible Expenses

The holidays are a great time to let loose and be more sociable with co-workers, clients, and referral partners. But just as you lose count of how many calories you're taking in, you can lose track of the money you're spending. Not only can this result in overspending, of course, but you can also be missing out on deductible expenses that will save you money in just a few months at tax time.

The holidays are a great time to let loose and be more sociable with co-workers, clients, and referral partners. But just as you lose count of how many calories you're taking in, you can lose track of the money you're spending. Not only can this result in overspending, of course, but you can also be missing out on deductible expenses that will save you money in just a few months at tax time.

Perhaps you're planning an office Christmas party for your staff. Not only would those expenses be deductible, even food purchased for a potluck, but any staff appreciation gifts you'd like to hand out, as well. The same goes for client or vendor appreciation gifts. (If you have someone external doing your books, be sure they're asking about purchases for things like massage gift cards and fruit baskets, and recording them as business expenses, not draw activity.)

Many networking groups hold a special holiday party. Not only would any food and drink you purchase for that be deductible, but also mileage to the event. If you're having trouble keeping up with your mileage, something as simple as a mileage log (free to download here) in your vehicle or as sophisticated as an app can do wonders to help you track that.

Whatever you do, be sure you're keeping proper record of your business expenses, even while you party it up.

Falling Behind on Bookkeeping

Between parties, travel, and employees being out sick from all the germs they picked up partying and travelling, it's easy for certain tasks to get a bit behind in the later part of the year. However, bookkeeping is not like cleaning the house; you can't just plan to catch it all up at once. If I don't clean my house for a month, it's not that much more difficult, proportionately, than if it's not cleaned for a week. Bookkeeping doesn't work that way. If your bookkeeping takes four hours a month and you fall three months' behind, you now have twelve hours worth of bookkeeping to do. (And finding twelve hours for a task you like is difficult enough; imagine trying to find half an entire day to dedicate to a task you dislike.)

Between parties, travel, and employees being out sick from all the germs they picked up partying and travelling, it's easy for certain tasks to get a bit behind in the later part of the year. However, bookkeeping is not like cleaning the house; you can't just plan to catch it all up at once. If I don't clean my house for a month, it's not that much more difficult, proportionately, than if it's not cleaned for a week. Bookkeeping doesn't work that way. If your bookkeeping takes four hours a month and you fall three months' behind, you now have twelve hours worth of bookkeeping to do. (And finding twelve hours for a task you like is difficult enough; imagine trying to find half an entire day to dedicate to a task you dislike.)

Many business owners who find themselves in the position of staring down months of untouched financials make the decision to get some outside help, just to catch things up. The problem is that they're in good company. Beginning in November, professional bookkeepers get very busy with new clients who are hoping to get their books cleaned up for year-end. Not only is there an influx of new clients, but existing clients continue to need service, and we're busy getting all of their year-end documents ready as well. Many of my friends who work solo or operate smaller firms do not take on any new work during this time of the year.

If you aren't certain that you'll be able to keep up with your financials on your own during the holiday season, begin seeking assistance now, before you get too busy.

Not Preparing for Next Year

(NOTE: If you are one of those people who files an extension out of habit, this is for you.)

You may not realize it, but there is a lot you can be doing right now to get ready for next year's tax season.

You may not realize it, but there is a lot you can be doing right now to get ready for next year's tax season.

Just like you don't have to wait to make a New Year's resolution to start getting fit, you don't have to wait for January 1st to start getting your books in shape for tax season. For starters, you can be preparing for the January payroll reporting rush. In the chaos of year-end, many business owners forget that 1099s and W-2s are due at the end of January, and not in April. To prepare, you can be sure that you have W-9s, W-4s, and any required state tax documents on hand now, instead of trying to get them from workers later. (This is especially true of 1099 contractors, as they may work for you for a much shorter season and can be harder to track down later.)

If you have been using an outsourced payroll system, be checking now to ensure that the payroll reports in your financials match those provided by the vendor. Sometimes errors do occur, and you will need to alert the payroll company right away if their totals are incorrect. (Like bookkeepers, they are getting very busy this time of year, too.)

You want to check to make sure that your sub-ledger totals, such as your Accounts Receivable and Accounts Payable, match your General Ledger balances. You also want to be sure that you are up-to-date on any reconciliations.

Finally, it's a good idea to take some additional tax-sheltering steps. For example, if you had a good year and are cash-basis, consider making a large business purchase in December instead of January, to reduce your taxable income. Or maybe you have not been paying enough into your withholdings or your quarterly estimated self-employment taxes, and need to increase those in December. There are many options available to you, but you need to act now.

Fortunately, you still have some time to make the most of your holiday season. Stay on top of your books as you go, and you will have a restful and relaxing January (at least compared to everyone who didn't put in the work during December). If you need help, we are always available.

How You Use ROI Every Day

For those who don't know, ROI stands for "return on investment". Colloquially, you might think of it as "bang for your buck". Though it's frequently used to describe investment decisions, ROI is something you use in your daily life. You go to the gym because the payoff of improved health has greater value than the time you put into it. You're getting a good return on that time invested.

You might even use ROI to compare two options. Let's say your goal is to lose fat, and there are two classes open when you go to the gym. You could go to an hour-long spin class, or an hour-long yoga class. Doing your research, you find that spin class burns 50% more calories, so you choose to go to that one, as it offers a better ROI.

Looking at it from a financial perspective, there's a very simple formula to calculate ROI.

Return on Investment = (Gain from Investment - Cost of Investment) / Cost of Investment

Now, when it comes to ROI in small business, people tend to think of it primarily in terms of sales and marketing. Before you run an ad or hire a marketing firm, you should be looking at whether the income you're likely to gain outweighs the amount you're about to spend. (For a more in-depth look at mistakes owners make in their marketing budget, see our prior article, Living a Lie: The mistakes that make entrepreneurs go broke.) If you are paying a marketing firm $10,000 a year and your sales only increase by $3,000, you're not making a good return on your investment. Likewise, if you hire a salesperson at base $45K + commission, and he only makes $15,000 in sales, he's probably not in the right position at your company. These are the sorts of obvious examples people think of when it comes to ROI in their business.

However, any business decision really comes down to a matter of ROI, and that is true for hiring an accountant, as well. We're constantly fighting the stereotype of accounting as a necessary evil, and one way to do that is to look at all the benefits that come with good bookkeeping and CFO.

First, of course, are the tax savings. Accurate books not only help you avoid an audit and costly penalties, but also aid you in tracking and recording every deduction for which you're eligible.

Second is saving on expenses. A good CFO service should be locating areas of overspending and helping you restructure to lower or even eliminate certain costs. (Actually, we tend to recommend you eliminate those expenses which don't produce a good ROI. See? It really does all come back to that.)

Third, we like investigate means of increasing revenue. This could be by introducing a new product or service line, acquiring another business, re-examining current pricing strategies, or even by locating and collecting on aged receivables.

To look at how The Bookkeeper does this from an ROI perspective, we save or earn our average client enough in our first year with them to pay our fees for 23 months. That's an almost 100% return on investment.

Finally, there are the benefits which are harder to quantify, primarily opportunity costs. What do you save in energy and stress by hiring someone to take over certain tasks for you?

This week, I challenge you to take a close look at your business, find what's paying off, find what's not, and do something about it.

Year in Review: Our clients' big wins in 2015

People tend to think of bookkeeping as a necessary evil. Your business has to have it, so just find someone who will do a decent job and whom you don't have to pay too much.

We beg to disagree.

We like to use our service to do more than just keep our clients' books clean. We like to go beyond balancing books to growing businesses. In that regard, 2015 was a very good year for us.

Today we want to showcase three clients who had big "wins" in the last 12 months.

C lient #1: A Money-Saving Solution

lient #1: A Money-Saving Solution

One of our client's businesses was facing some difficulties staying profitable. Looking at the books, we found some areas where expenses were duplicated and some cases of fairly extreme overspending. We met with the owner and devised a plan to cut expenses. Once the plan went into effect, we were able to increase the bottom line by over $30,000 a month.

Of course...big deal, right? Everyone knows accountants are penny-pinching killjoys. Let's look at our second story, and see how we can help a client without forcing them to spend less.

Client #2: A Long-Denied Loan

A different client desperately desired a consolidation loan. He had gone to three different lenders, and been denied each time. He was getting nowhere in a hurry.

So, we took over.

First, we received authority to act on his behalf. Then we got to work, combing through his financials and organizing the data for presentation. Finally, we were able to present the information to the bank in the way we knew they wanted it. This time it was approved, and we were able to get our client a consolidation loan at one of the same institutions who had previously rejected him.

Thanks to those efforts, our client was able to consolidate his debt under one payment, and greatly improve his cash flow.

Still, that story isn't as great as...

Client #3:  Money from Thin Air

Money from Thin Air

Sometimes, something as simple as developing better procedures can make all the difference to a business. This was the case with a client who didn't have a good system in place for managing A/R.

Specifically, there was over $102,000 in receivables of which the owner was not even aware. (Some of the unpaid invoices were over two years old.)

When we discovered this large balance of aged receivables, we immediately began developing collections procedures, including a series of formalized letters to the debtors. Using the practices we put into place, over $30,000 has been collected within the last four months, with payments continuing to roll in.

To re-cap, that's money that the client did not even know existed.

These are just a few of our highlights from 2015. We can't wait to see what we do in 2016.

Managing Accounts Receivable: Because sales are meaningless when clients don't pay you.

In order to stay competitive, many business owners find it necessary to extend credit to customers. However, if you offer later payment options, it is crucial that you have a well-developed and communicated accounts receivable system.

Here we have listed a few elements of a successful A/R management plan, and how to implement them in your business.

Communication. It's said to be the key to a good relationship, and that can apply to business relationships as well as personal ones. Communicating well is key to managing receivables accounts. Let's look at the who, what, when, and how, of A/R communications.

Who? This seems obvious, enough...the customer, right? But, in reality, it's not just the customer with whom you are communicating. Assuming you're not a 1-person operation, you need to be in good communication with your employees or co-workers regarding what promises and agreements have been made with the customer. If you contact a customer on Tuesday afternoon regarding a past due invoice, and they just told your partner that morning that the check is in the mail, your entire company looks disorganized and unprofessional.

What? When alerting a customer to a past due payment, simply informing them of the amount owed is not the best option. Providing a detailed statement, possibly with an itemized duplicate of the referenced invoice, is far more helpful. Important information to include is the amount owed, days past due, what services were rendered, options for remitting payment, and contact information for questions regarding the account.

When? Generally, you would expect to increase contact as balances get further past due. A gentle reminder the day after the due date if payment has not yet been received is appropriate, with missives gradually becoming more frequent and insistent as the invoice gets to 15 days past due, 30 days past due, etc. (However, it would be best to avoid multiple communications a day, as that could constitute harassment.)

How? "The medium is the message". For an account that is just barely overdue, a mailed or emailed statement (as described above) might be enough of a reminder. If more time passes without payment or a response from the customer, a more direct phone call is in order. This leads us to our next element of a successful accounts receivable management system...

Delegation. To maintain a good working relationship with the customer, it is ideal if you can separate the less pleasant side of that relationship, collections, from the more positive side, which is the work and value you provide to the client.

Delineating separate avenues of communication between the service and payment sides of your business can help you achieve your A/R management goals without damaging the rapport you have built with your client. Large companies have entire Accounts Receivable departments, but small businesses rarely have that option.

However, if you have more than one employee, someone other than the client's primary contact could act as the accounts receivable delegate. If you're the sole employee, you can even do something as simple as set up a separate email. (For instance, if your email is "[email protected]", you could set up an email called "[email protected]".)

The key is to avoid marring interactions with the customer which could lead to continued or future work by derailing the conversation into payment discussion.

Documentation. Good documentation can prevent so many problems in every area of business, but especially in accounts receivable. Before a single customer is invoiced, your A/R plan should be formulated and written down so everyone in your business knows exactly what the payment terms are, who is responsible for contacting customers, what to do in case of a dispute, etc.

Payment terms should be made clear to the customer before services are rendered, and should then be reiterated on the invoice. If a balance does become overdue, remind customers of the payment terms, and document every communication with the customer regarding the overdue balance. Reference previous conversations about the account in new discussions about them. Established fact is far more effective in encouraging remittance than strong emotions or harsh words.

What should you do with a customer who isn't paying?

If the customer hasn't gone ghost on you (in other words, if they are still maintaining some form of contact with you), and would like to continue purchasing goods or services from you, do not cut them off. Cutting them off completely is a great way to ensure that they will do no further business from you, and will not pay you the money already owed.

However, do not provide any further service on credit. Request pre-payment for any further work you perform, then apply that payment to their outstanding balance. This allows you to maintain a working relationship with the customer and recoup the money you are owed.

The Financial Reasons Small Businesses Fail

Almost every entrepreneur has heard the statistic: 80% of small businesses fail. There are many reasons this happens, and can include everything from market slumps to lazy owners. To enumerate every way a business can go under would be an endless, impossible task.

However, there are a few financial characteristics frequently found in struggling businesses. Here are the most common financial reasons small businesses fail.

There's no plan. It's not uncommon to meet new small business owners who have a brilliant product idea, a well-developed marketing plan, a slick website, and not one thought given to their budget. We've already written on the tough financial questions to answer before starting your own business, but the importance of a solid financial bedrock cannot be overemphasized. A well-researched budget and fixed goals is the key to surviving that crucial first year in which most businesses go under. Great customer service and spot-on marketing are not enough to balance out shaky financials.

Speaking of customer service...

Poor credit management and pricing strategies are bad for everyone. No one craves popularity like an entrepreneur and, when your business's success is entwined with how well-liked you are, the urge to avoid offending anyone becomes even stronger. In the early days of a business, when there are only a few customers, there is a common impulse to let clients slide on late payments, or to offer frequent "friends and family" discounts. It's easy to justify this with the logic with the idea that you need to establish customer loyalty, and you can tighten the reins a bit when you have a solid customer base. There are a few reasons this doesn't work:

- Clients who don't pay on time aren't going to appreciate the slack you've given them in the past; they are going to resent the restrictions you enforce in the future.

- Likewise, your patrons who are just coming to you for the lowest price will quickly go elsewhere when your rates rise.

Lenient accounts receivable and cheap pricing might gain you a quick boost in early sales, but they are not a sustainable model. Delivering a product you can be proud of, at a price that is worth your hard work and can keep your business afloat (and actually requiring customers pay you that fair price) ensures that your customers the pleasure of patronizing your business for years to come. Because you have to remember...

Cash is king. Yes, it's a cliche, but that doesn't make it any less true. A great business model matters little if you run out of money before you can implement it. Managing cash flow is key to not just the health but the continued existence of your business. Here are a few of the most common cash pitfalls small businesses face:

1.) Insufficient capital. In all likelihood, your business will not be immediately profitable. So not only do you need enough cash to get your business started, but you need enough to allow yourself to operate at a loss for a while.

2.) Not having a large enough cash cushion. Think "Princess & the Pea" levels of padding. Regardless of how well you plan, the economy is unpredictable. Look to history for examples. No one expected the Boston Molasses flood which, in addition to the damage caused and lives lost, resulted in a nearly $11M settlement (in today's money) for the responsible company.

3.) Over-investing in fixed assets. It's great to plan for the long-term but, if you don't plan for the short-term as well, your business will not get a long-term. Sacrificing too much of your cash for something like manufacturing equipment (even if you're getting a great deal) can hurt you, as that is not a liquid asset and will be of no help to you in the event of an emergency (i.e. your factory flooding a major metropolis with 2.3M gallons of molasses). Think of it like a game of Monopoly; if you start building hotels too soon and suddenly need cash, you're stuck selling all your buildings back to the bank for half-price, and you know bankruptcy is right around the corner. Only, in real business, instead of losing yet another game to your annoying brother-in-law, you've lost your entire livelihood.

Expanding your business is the ultimate goal, but maintaining cash flow gives you the solid foundation you need to build upon.

80% of new businesses fail, but that means 20% succeed. To be that 1 out of 5, have a plan, know your value, and remain patient. Better to start small and grow something big than to start too big and dwindle away.